Market Update: Blockbuster

US equity indexes were up on the week: S&P500 +1.4%, NASDAQ +1.1%, and DJIA +1.4%. Year-to-date, equity indexes are well in the green: S&P500 +4.0%, NASDAQ +4.1%, and DJIA +2.6%. Friday's January US payrolls data were blockbuster - well exceeding the consensus estimate (see below). The data are sign that US economic exceptionalism is continuing. US equity indexes rallied on the strong economic news and US Treasury yields surged in reaction. The US 2 year and 5 year yields were up about 20bps and the 10 year yield 17 bps post-release. They ended the week: 2 year: 4.3638%, 5 year: 3.9825%, 10 year: 4.0199%

US Economic Data, January FOMC, and Fed Pricing:

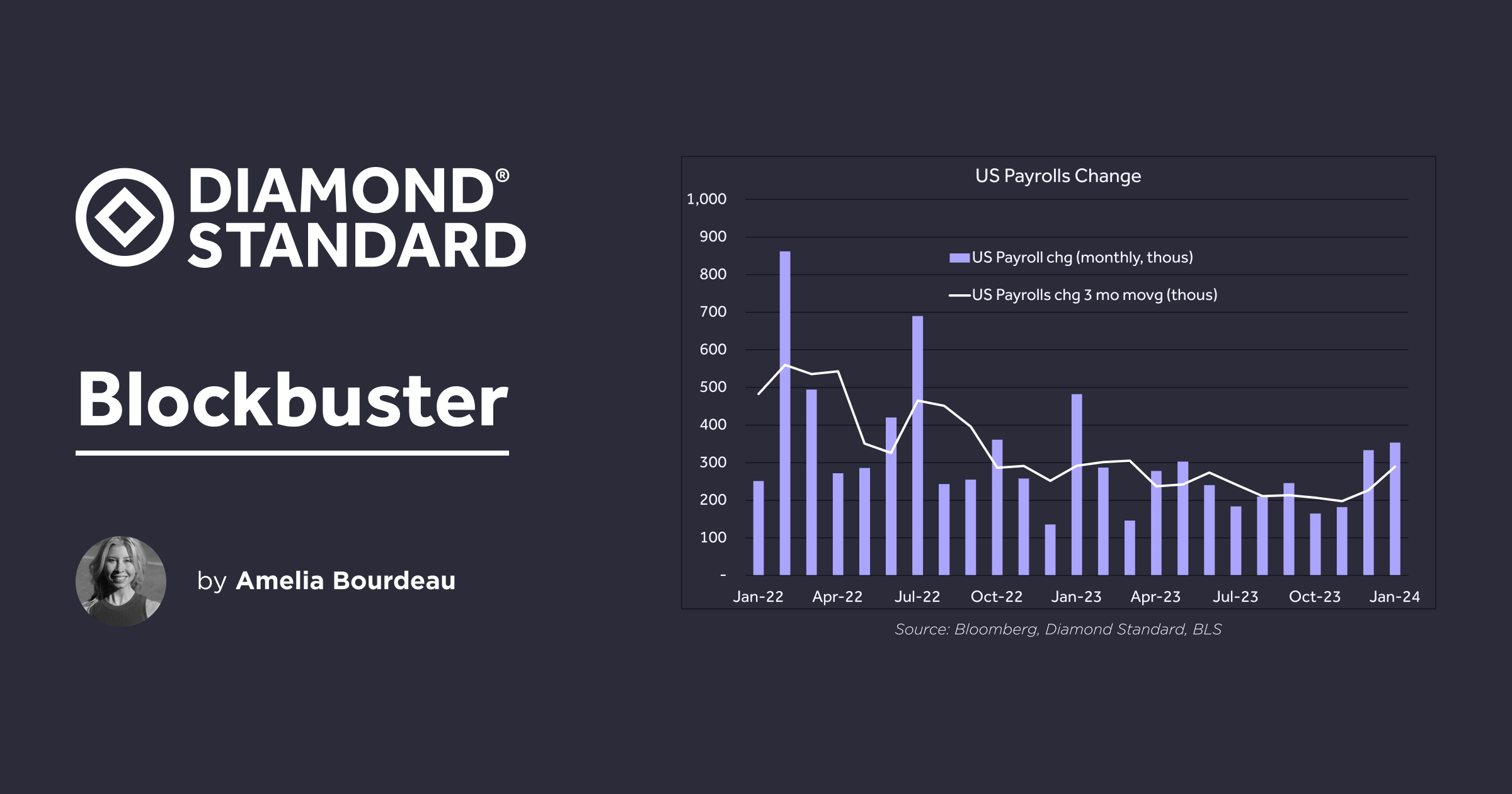

January US payrolls surprised strongly to the upside, rising 353k vs expectations of 185k. In addition, December payrolls were revised up 117k to 333k. The unemployment rate held steady at 3.7% vs expectations that it would rise to 3.8%. It has been sub-4.0% since February 2022. January average hourly earnings were strong, rising 0.6% m/m - well above the consensus expectation of 0.1% m/m. On a year-on-year basis, they were up 4.5%, an increase from 4.3% y/y in December.

At the January FOMC meeting, held prior to the payroll release, voting members held the target range for the fed funds rate at 5.25% - 5.50% as expected. The most important result to come out of the meeting was that the FOMC committee removed its implicit tightening bias from the statement.

However, at Fed Chair Powell's press conference, he did not signal a rate cut was imminent at the upcoming March FOMC meeting. He was careful to emphasize that the Fed needs greater confidence that inflation is moving "sustainably toward 2 percent." Powell stated that he did not think that level of confidence would come by the March FOMC meeting and that a March rate cut is "not the most likely case" or "base case."

Fed funds futures are pricing in approximately 122 bps of easing in 2024, which is about five 25bp rate cuts. By comparison, the Fed is forecasting three 25bp rate cuts for 2024. There is now a 19% probability of a 25bp cut priced in for the March FOMC, which is down notably from one week ago when it stood at a 46% probability. Given Powell's comments at the press conference and the newly accelerating labor and average hourly earnings data, it is unlikely the Fed can deliver a rate cut in March.

Chart: US Payrolls monthly change and 3 month moving average. Payrolls are re-accelerating.

Precious Metals:

We continue to favor an allocation to precious metals including the diamond commodity for diversification and safe haven purposes. Geopolitical tensions and global elections, which include the US presidential election, could keep financial markets volatile this year, creating demand for precious metals as a hedge. Fed easing should help support gold and silver while a strong to steady US consumer is a positive for the diamond market.

Diamond Industry Starting 2024 on a Positive Note

DIAMINDX is up 3.8% to USD 4,350 from its low the first week of November 2023. There is a deeper dive into the DIAMINDX price movement with S&P Global here. The natural diamond industry is emerging from the supply overhang which hindered it in 2023 after two years of record consumer diamond demand. The industry is starting 2024 with a sense of equilibrium.

The DeBeers Group announced the value of rough diamond sales for 2024 Cycle 1. Sales rose USD 370 million, falling 19% y/y but up strongly from the previous cycle's (Cycle 10 2023) result of USD 137 million at which DeBeers offered lower supply.

Al Cook, CEO, De Beers Group, said: “Solid consumer demand for diamonds in the United States over the year-end holiday season has certainly helped to stabilise the industry and we are seeing polished diamond prices increasing again. Combined with the restart of rough diamond imports into India, this has led to demand for rough diamonds increasing substantially in the first sales cycle of 2024. However, as the prospects for economic growth in many major economies remain uncertain, we expect that it may take some time for rough diamond demand to fully recover."

As the US is world's largest market for diamonds, the US jewelry industry is focused on the upcoming Valentine's Day holiday. The National Retail Federation ("NRF") predicts total spending to reach USD 25.8 billion for Valentine's Day, which includes USD 14.2 billion in spending on significant others - a record high. USD 6.4 billion is expected to be spent on jewelry. The NRF survey states, "Consumers expect to spend $185.81 each on average, nearly $8 more than the average Valentine’s Day spending over the last five years...This year, while consumers still value the non-romantic relationships in their lives, they are prioritizing gifts for significant others." These figures demonstrate the continued strength of the US consumer and strong jewelry demand - both a plus for the diamond industry.

Gold and Silver

Gold fell 1.1% in January. At the time of writing, XAUUSD is at USD 2,036. It has been in a USD 2,062-2,002 range since the start of the year, remaining above key support at USD 2,000. Silver rose 3.65% in January. XAGUSD is at USD 22.63 as of Friday mid-day NY and has been trading in a USD 22.00-23.40 for the year so far. Both gold and silver fell in reaction to Friday's strong US jobs report.

The World Gold Council ("WGC") released its report 2023 Central Bank Gold Statistics. Central bank gold buying continued in December. Net purchases for the month were 28t. For 2023, central bank gold purchases were strong. Annual net purchases were 1,037t, falling just 45t short of the 2022 record. 2023 was the second consecutive year of net purchase above 1,000t. The People's Bank of China ("PBOC") and the National Bank of Poland were the largest buyers. The Central Bank of Uzbekistan and the National Bank of Kazakhstan were the largest sellers (according to data at the time of writing). See chart below. The WGC noted that the PBOC's net purchase of 225t in 2023 is its "highest single year of reported additions since at least 1977." The Monetary Authority of Singapore was the sole developed market buyer as the ECB buying was related to "Croatia joining the Eurozone in January." The WGC expects central bank buying of gold to continue "at an impressive rate" in 2024.

Chart: Central Banks - largest net purchases/sales in gold (tonnes) in 2023

USD

USD (DXY Index) rose 1.9% for the month of January and is currently at 103.27. This week, the DXY Index rose on the back of strong US economic data which has pushed back market pricing for the first Fed rate cut. It has been trading in a relatively tight 104.00-103.00 range since mid-January. This is well within the wider range of 107.00-100.00 that the USD has been holding in since July 2023. The USD appreciated against all G10 currencies in January.

JPY was the weakest currency vs USD in January, falling 4.4%. USDJPY is topside 148.00 to start the month of February and is responding to higher US front end yields. EURUSD, the DXY Index's largest component, fell 1.9% in January. It was down approximately 0.6% on the week in reaction to both Fed Chair Powell's press conference and the stronger than expected US payroll data. At the time of writing, the single currency is at 1.0786 breaking once again sub - 1.0800.

The Fed, ECB and BoE seem to be struggling with deciding when to commence a rate cutting cycle. Economic outperformance continues to support the USD in contrast to sluggish Eurozone and UK economies. Looking ahead, the USD could also be further supported if some of rate cuts for 2024 are priced out.

Chart: USDJPY vs US 2 year yield - 3 day. The move up in US short term yields drove USDJPY higher on Friday.

Ahead:

Fed chairman Powell will appear on CBS News 60 Minutes Sunday evening to discuss inflation, expected rate cuts, and the banking system. The network said that the interview was taped prior to the January jobs report release.

The US ISM services data for January are released next week. Market participants will continue to keep their eyes on US initial jobless claims to monitor the employment market. There is a handful of central bank speak from both the ECB and BoE next week.

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.