Market Update: Plenty of Runway

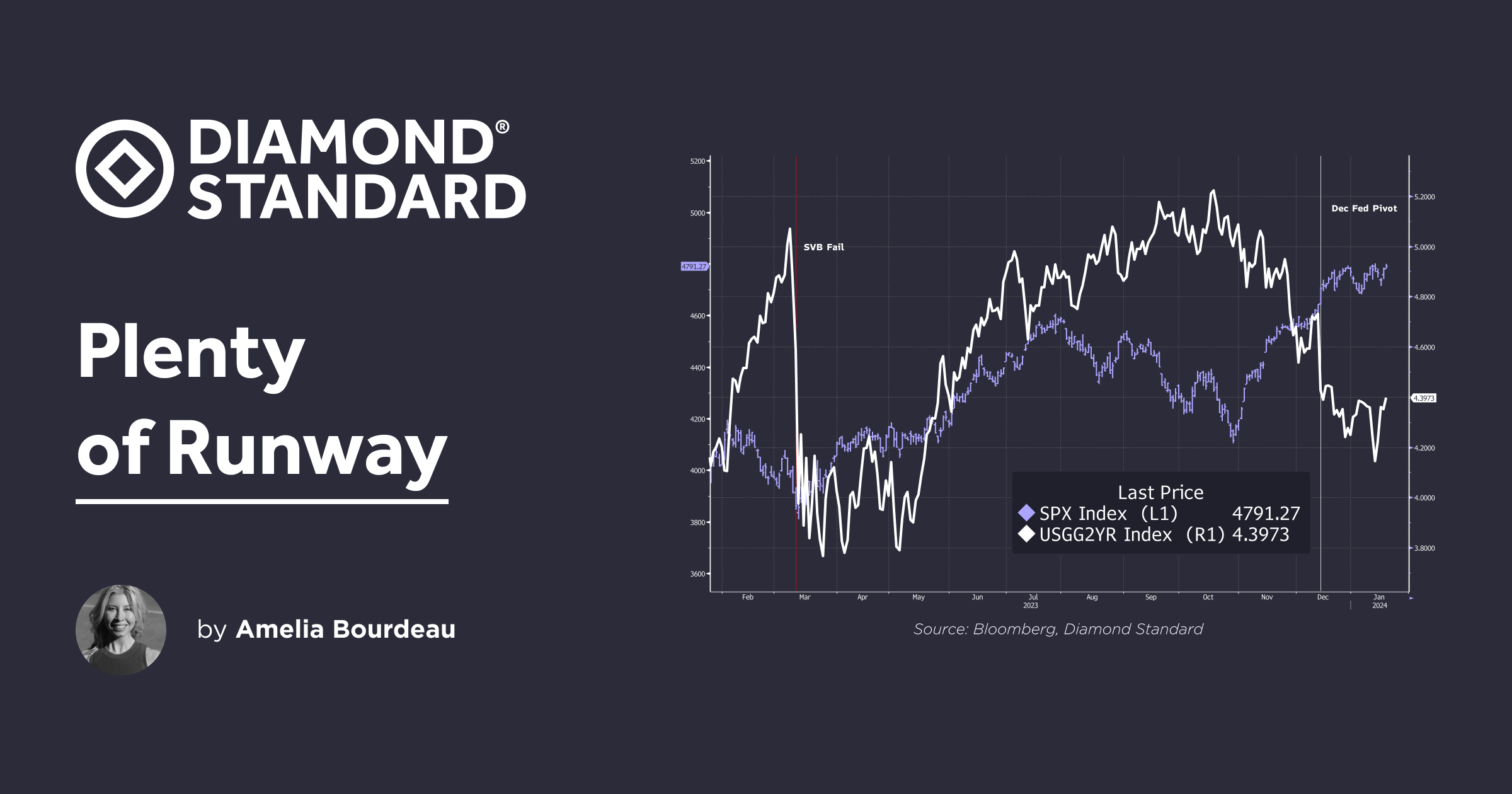

US equity indexes were up on the week: S&P 500 +1.2%, NASDAQ +2.3%, and DJIA +0.7%. The S&P 500 closed at 4,839.81 - a record high. Year-to-date, US equity indexes are more subdued than their strong run-ups into year-end 2023, but are in positive territory. YTD: S&P 500 +1.5%, NASDAQ +2.0%, and DJIA +0.5%. With US economic data remaining solid and the Fed signaling a rate cutting cycle this year, it looks like the economy has plenty of runway to achieve its soft landing. That is, in fact, the consensus view. This combination of factors is also supporting risk seeking.

US Economic Data and Fed Pricing:

Overall, US economic data are positive. This week, December retail sales were released and showed that consumer spending picked up into the year-end. Retail sales rose a strong 0.6% m/m and 5.6% y/y for the headline an 0.4% m/m and 4.5% y/y ex auto. On Thursday, initial jobless claims came in at 187k, which is the lowest read since September 2022 and a sign that the labor market remains solid.

Last week, December headline CPI came in higher than expected, rising to 3.4% y/y from 3.1% y/y in November driven by higher energy prices. However, core CPI ticked down to 3.9% y/y for its first sub - 4.0% reading in two and a half years. Friday's University of Michigan January consumer sentiment report showed that consumers' price expectations eased further for both the short and long term measures with short-term expectations falling to the lowest since December 2020.

The Fed surprised market participants at the December FOMC meeting, delivering the much awaited "pivot" toward rate cuts in its Summary of Economic Projections ("SEP"). The December SEP forecasted three 25bps rate cuts for 2024. By comparison, fed funds futures are pricing 143bps of easing for 2024, which equates to about six 25bp rate cuts. There is a 52% probability priced that the Fed will ease 25bps at its March policy meeting. The next FOMC announcement is January 31st and no change in the policy rate is expected at that meeting.

Chart: US 2 year yield vs S&P 500

Precious Metals

We continue to favor an allocation to precious metals including the diamond commodity for diversification and safe haven purposes. Geopolitical tensions and global elections will likely keep investors keen on precious metals. The Associated Press reports that over 50 countries which represent approximately half of the world's population will have elections this year. Those elections include, of course, the US presidential election. Financial markets dislike uncertainty and so investors could look to precious metals as a hedge. In addition, expected Fed easing should help support gold and silver while a steady US consumer is a positive for the diamond market.

Diamond Industry Starting 2024 on a Positive Note

DIAMINDX is up USD 200 to USD 4,390 from its low the first week of November 2023. The natural diamond industry is emerging from the supply overhang which hindered it in 2023 after two years of record consumer diamond demand. The industry is starting 2024 with a sense of equilibrium. In Anglo American's year end investor update, CEO Duncan Wanbland said of DeBeers Group, "we believe that the current weakness [in diamond demand and prices] is temporary... Already, there are some signs that the market is beginning to turn."

The novelty of lab grown diamonds has perhaps begun to wear off as more consumers realize that they do not hold their value and can not be used as an asset - a factor that, according to industry analysts, is an important consideration in the bridal space. The narrative in the press regarding lab grown diamonds has shifted in a less positive direction. The Wall Street Journal wrote an article titled "The Embarrassment of Having to Explain Your ‘Monster’ Diamond Ring."

Turning to rough diamonds, the DeBeers Group offered lower rough diamond supply at its last sales cycle of 2023 held in December. CEO Al Cook stated:

"...we are seeing signs that the diamond industry is regaining its balance between wholesale supply and demand. Polished diamond prices look to have stabilised as inventory levels have decreased, though we expect improvements in rough diamond trading conditions to be gradual.”

This week, the DeBeers Group held its first rough diamond sale of 2024. While results have not been released yet, Bloomberg News reported that DeBeers reduced prices of its rough diamonds by 10% "to stimulate the market," citing sources familiar with the tender. This is in line with Cook's assessment that the recovery in rough diamonds would be gradual - DeBeers is likely trying to incentivize demand temporarily at the start of the year especially if it increased supply at this first 2024 tender.

The G7 plus European Union sanctions on the importation of diamonds directly from Russia commenced January 1st. On March 1st these sanctions will be expanded to include Russian diamonds that have been substantially transformed in another country (such as cut and polished in India). From September 1st the sanctions will be expanded again to include lab grown diamonds and jewelry and watches containing diamonds.

The G7 statement noted that for G7 members who are major importers of rough diamonds, "a robust traceability-based verification and certification mechanism for rough diamonds" will be established. Furthermore, the G7 will continue to consult with diamond producing and manufacturing countries regarding comprehensive controls relating to traceability for diamonds produced and processed in third countries." The diamond industry awaits clarity on the implementation of the March 1st and September 1st sanctions.

A Question and Answer document from the European Commission suggests that the blockchain will be used to track diamonds: "the traceability system includes a mandatory registration, using so called ‘digital twins' of the real diamond in its rough state and issuing a certificate of its origin. The identifying information and certificate will be entered in blockchain-based ledger. This allows the diamond to be traced through the production process and can be presented at the time of importation of the finished diamond."

These sanctions will further limit diamond supply to consumers in the G7 nations, who, according to the US State Department, account for approximately 70% of all diamond purchases.

Gold and Silver

Gold and Silver are down 1.3% and 5.0% respectively on the year so far. Gold as of Friday at USD 2,033 remained above key support at USD 2,000 - a threshold it has held above since mid-December. Silver currently at USD 22.52 has held above USD 22.00 support. Recent US economic data have surprised to the upside and, as a result, front-end rates are higher which has weighed on both gold and silver.

For 2023, Gold (XAUUSD) rose 13% and silver (XAGUSD) fell 0.7%. Gold's resiliency in 2023 was somewhat unexpected given rapidly rising interest rates and strong US economic growth. The World Gold Council ("WGC") notes in its 2023 Review that emerging market central bank demand was a significant contributor to gold's rise along with elevated geopolitical risk. Both helped to mitigate the drag from higher interest rates. Looking ahead, in its Gold Outlook 2024, the WGC brings up the point that "Historically, soft landing environments have not been particularly attractive for gold, resulting in flat to slightly negative returns." But that could have been said for 2023 as well. 2024 will see continued heightened geopolitical tension and election risk. The floor in the gold price will depend on continued central bank buying and any further rise will likely need participation from institutional investors.

Chart: XAUUSD vs US 2 year yield (rs, inverted)

__USD __

USD (DXY Index) is up approximately 2.0% on the year to 103.51, remaining well within the 100.00 - 107.00 range that it has been since early 2023. The USD has appreciated against all G10 currencies on the year so far. It is largely being driven by changing expectations and pricing of Fed rate cuts. It is not clear that the USD would weaken on a sustained basis when the Fed commences its rate cutting cycle as the cuts are all ready priced and the USD reflects this. Any easing priced out on stronger than expected US economic data could support USD. In addition, from a relative value perspective, the market participants expect the ECB and BoE to follow the Fed with rate cuts starting in Q2 2024.

EURUSD, the DXY Index's largest component, has been holding in a 1.1000 - 1.0850 range since the start of the year. At the time of writing EURUSD is 1.0880. There is no catalyst for EURUSD currently, but the eurozone remains on its back-foot in terms of economic growth compared to the US. The long awaited possibility of a BoJ rate hike has been pushed back once again as its December CPI report supported the view that there is no need to rush into hiking as price pressure is easing. USDJPY has risen back to the 148.32 area after trading down to 140.90 on USD weakness following the Fed's December pivot.

Chart: DXY Index 107.00 - 100.00 range

Ahead

Next week, US Tier 1 economic data releases include: Q4 US GDP, December personal spending and income, and December PCE prices. There is no Fed-speak ahead of the January 31st FOMC rate decision and press conference. The ECB, BoC, and BoJ have monetary policy meetings.

Disclaimer:

This report has been prepared by the Strategy Team of Diamond Standard Inc. (“Diamond Standard”). This report, while in preparation, may have been discussed with or reviewed by persons outside of the Strategy Team, both within and outside Diamond Standard. While this report may discuss implications of legislative, regulatory and economic policy developments for industry sectors, it does not attempt to distinguish among the prospects or performance of, or provide analysis of, individual companies and does not recommend any individual security or an investment in any individual company and should not be relied upon in making investment decisions with respect to individual companies or securities.

Opinions and estimates offered constitute our judgement and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. Under no circumstances does the information contained within represent a recommendation to buy, hold or sell any security, and it should not be assumed that the transactions discussed were or will prove to be profitable.